Beyond the Balance Sheet: The Five Dimensions of Family Wealth

The roots of the word “wealth” trace back to wela, Old English for “well-being.” It’s a telling origin—one that suggests wealth was never meant to be just financial. For families navigating succession, stewardship, and purpose, reclaiming that broader definition might be the most valuable inheritance of all. At Beacon Family Office with Assante Financial Management Ltd., we believe true wealth includes the ability for families to live well—together and across generations.

While financial capital is important, it’s only part of the story. When guided by purpose, wealth becomes a way to support what matters most: relationships, values, and impact that endures.

The Stewardship Shift: From Preservation to Activation

Many families begin their planning journey focused on preservation—minimizing taxes, reducing risk, and avoiding loss. While these conversations are essential stepping stones, they often represent only the starting point of true family stewardship.

Stewardship invites a broader perspective. It encompasses the intentional care and activation of family capital to build capacity across generations. This shift—from simply protecting assets to thoughtfully activating them—allows families to use today’s resources to enhance their collective well-being for years to come. Effective stewardship might include establishing family education initiatives, creating meaningful philanthropic engagement opportunities, or developing governance frameworks that evolve with the family. When families move from asking, “How do we keep what we have?” to “How might we grow what matters most?” new possibilities emerge that benefit both current and future generations.

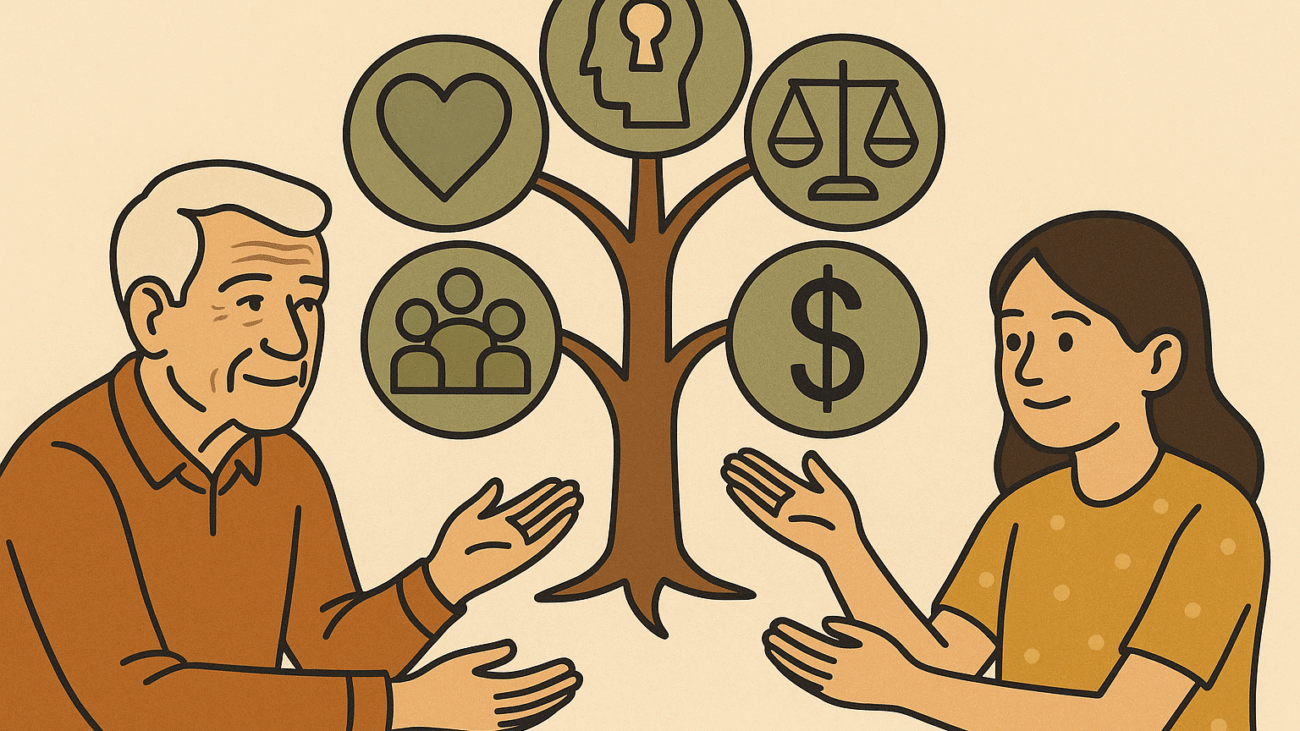

The Five Dimensions of Family Wealth

Drawing from the work of James E. Hughes Jr., we guide families to consider five core dimensions of wealth that look beyond financial assets. Human, intellectual, social, spiritual, and financial capital work together as interconnected elements of a family’s true wealth. These dimensions, when stewarded thoughtfully and in harmony, create a foundation of clarity, capability, and cohesion that can sustain a family across generations. Our approach helps families build lasting confidence by intentionally nurturing each of these dimensions, creating a holistic framework that supports both individual growth and collective purpose. Let’s dive in and understand each of these dimensions as they might apply to your family business:

- Human Capital: Investing in People

Human capital represents each family member’s capacity to thrive through personal growth, emotional intelligence, leadership development, education, and overall well-being. At Beacon Family Office, we align financial plans with personal development goals, treating investment in people as foundational to family success. To actively steward human capital, families can establish regular check-ins focused on individual growth aspirations, create educational stipends that encourage lifelong learning, and design family gatherings that intentionally develop leadership skills across generations.

2. Intellectual Capital: Preserving Wisdom that Lasts

Intellectual capital comprises the family’s collective knowledge, governance systems, shared stories, and learning capacity. We help families formalize decision-making processes, clarify roles, and prepare the rising generation for meaningful participation—preserving essential knowledge and insight alongside assets. Families can steward this dimension by documenting family stories and lessons learned, establishing clear governance protocols for joint decisions, and creating mentorship pathways where experienced family members can transfer knowledge to rising generations.

3. Social Capital: Strengthening Connection and Contribution

Social capital encompasses family relationships, community engagement, and reputational trust. We help foster intentional communication, align philanthropy with values, and create connection opportunities across generations. These strong relationships provide the cohesion that sustains family wealth over time. To strengthen social capital, families can implement regular communication forums where all voices are heard, develop shared philanthropic initiatives that reflect collective values, and create opportunities for cross-generational collaboration on family projects or community engagement activities.

4. Spiritual Capital: Leading with Purpose and Shared Values

Spiritual capital reflects the family’s shared principles and deeper purpose—why they steward together, what they stand for, and what legacy they’re committed to living. We help embed these values into investment decisions and transition strategies, strengthening unity when choices become complex. Families can nurture spiritual capital by articulating shared values in a family mission statement, aligning investment policies with these values, and creating space for regular reflection on how family resources are supporting meaningful purpose.

5. Financial Capital: Fueling the Vision with Precision

Financial capital enables growth across all other dimensions when deployed intentionally. We guide families in creating structures that reflect their goals and governance frameworks, positioning financial resources as strategic enablers rather than end goals. Effective stewardship of financial capital involves establishing clear investment policies that reflect family values, creating appropriate transparency around financial matters, and developing financial literacy programs that prepare all family members for responsible participation.

Confidence Is the Real Return on Stewardship

The most successful families we work with have made the deliberate journey from wealth accumulation to wealth activation. These families measure their progress through multiple lenses—the strength of their relationships during challenging decisions, the clarity with which family members communicate across generations, the readiness of rising family members to participate meaningfully, and the alignment between stated values and actual structures.

We’ve observed that families who regularly engage in multigenerational learning activities tend to approach complex decisions with greater confidence. Similarly, those who establish clear communication forums often navigate transitions more smoothly than those who focus primarily in wealth planning. These practices build a foundation of trust that becomes particularly valuable during periods of change or uncertainty.

When a family can approach complex decisions with clear processes and aligned values, they experience the true confidence that comes from effective stewardship across all dimensions of family wealth.

Concluding Thoughts

By stewarding all five dimensions of wealth, we help families create clarity, build capability, and deepen confidence in every chapter of their legacy. Wealth alone does not define a legacy. The way it is, stewards do.

Are you ready to move beyond preservation to activation? At Beacon Family Office with Assante Financial Management Ltd., we begin with a Family Wealth Dimensions assessment that maps your current stewardship strengths across all five capitals. This personalized evaluation creates a foundation for meaningful conversation about your family's next chapter. Contact us to schedule your assessment and take the first step toward confidence-based stewardship.

ABOUT THE AUTHOR

As the Senior Wealth Advisor at Beacon Family Office at Assante, Cory Gagnon has supported successful family enterprises to preserve, protect and transition their wealth since 2011.

Cory’s personal objective as a Wealth Advisor is simple. He is committed to supporting families to take control of the areas of their lives that truly matter to them. This commitment revolves around using specific tools and strategies that enable families to take action with confidence which will support them through life’s critical transitions.

ABOUT THE AUTHOR

As the Senior Wealth Advisor at Beacon Family Office at Assante, Cory Gagnon has supported successful family enterprises to preserve, protect and transition their wealth since 2011.

Cory’s personal objective as a Wealth Advisor is simple. He is committed to supporting families to take control of the areas of their lives that truly matter to them. This commitment revolves around using specific tools and strategies that enable families to take action with confidence which will support them through life’s critical transitions.